Das Center for Financial Studies betreibt unabhängige Forschung in wichtigen Bereichen der Finanzen.

Forschungsbereiche

Das Center for Financial Studies betreibt unabhängige und international orientierte Forschung zu wichtigen Themen im Bereich der Finanzen. Es dient als ein Forum für den Dialog zwischen Wissenschaft, Politik und Finanzindustrie. Es bietet zudem eine Plattform für hochkarätige Grundlagen- sowie angewandte Forschung mit Bedeutung für den europäischen Finanzsektor.

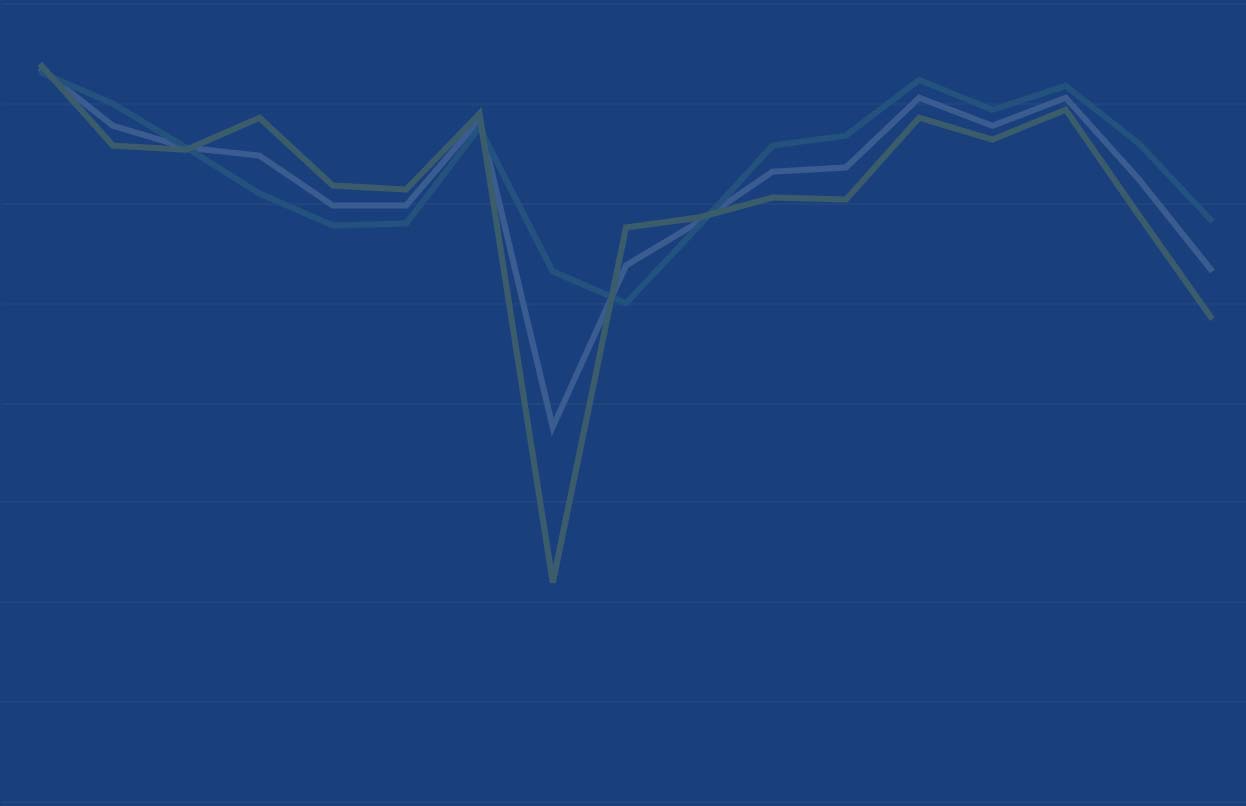

CFS Index

Der CFS Index Chart nutzt Technologien von Google. Um den Chart anzuzeigen, klicken Sie auf den unteren Button und bestätigen die Verwendung externer Medien in den Datenschutzeinstellungen.

Letzter Stand: 106.5

Aktueller Stand: 107.2

Letzte Umfrage:

12. – 19. Feb. 2024

Nächste Umfrage:

TBA

Hauptförderer